FS-2025-0788 | March 2026

Federal Student Loan Reform 2025-2028: Your Guide to Repayment, Forgiveness, Borrowing Limits, and What You Need to Do

By Dorothy Nuckols, MPH, AFC

What’s Happening

Federal legislation signed July 2025 called the One Big Beautiful Bill Act (OBBBA) is changing how federal student loans work. It affects current and future federal student loan repayment plans, loan forgiveness programs, and graduate borrowing limits. These changes are designed to simplify student borrowing and loan repayment, but they also alter benefits and narrow repayment options. If you are a student, graduate, or parent borrower, it’s important to understand how these changes impact you.

Some changes went into effect immediately in July 2025, like expanded access to the Income Based Repayment (IBR) plan. Others will roll out between 2026 and 2028, including the launch of a new repayment plan and new borrowing caps. This guide walks you through the changes and what steps you can take to stay on track.

Brief Background

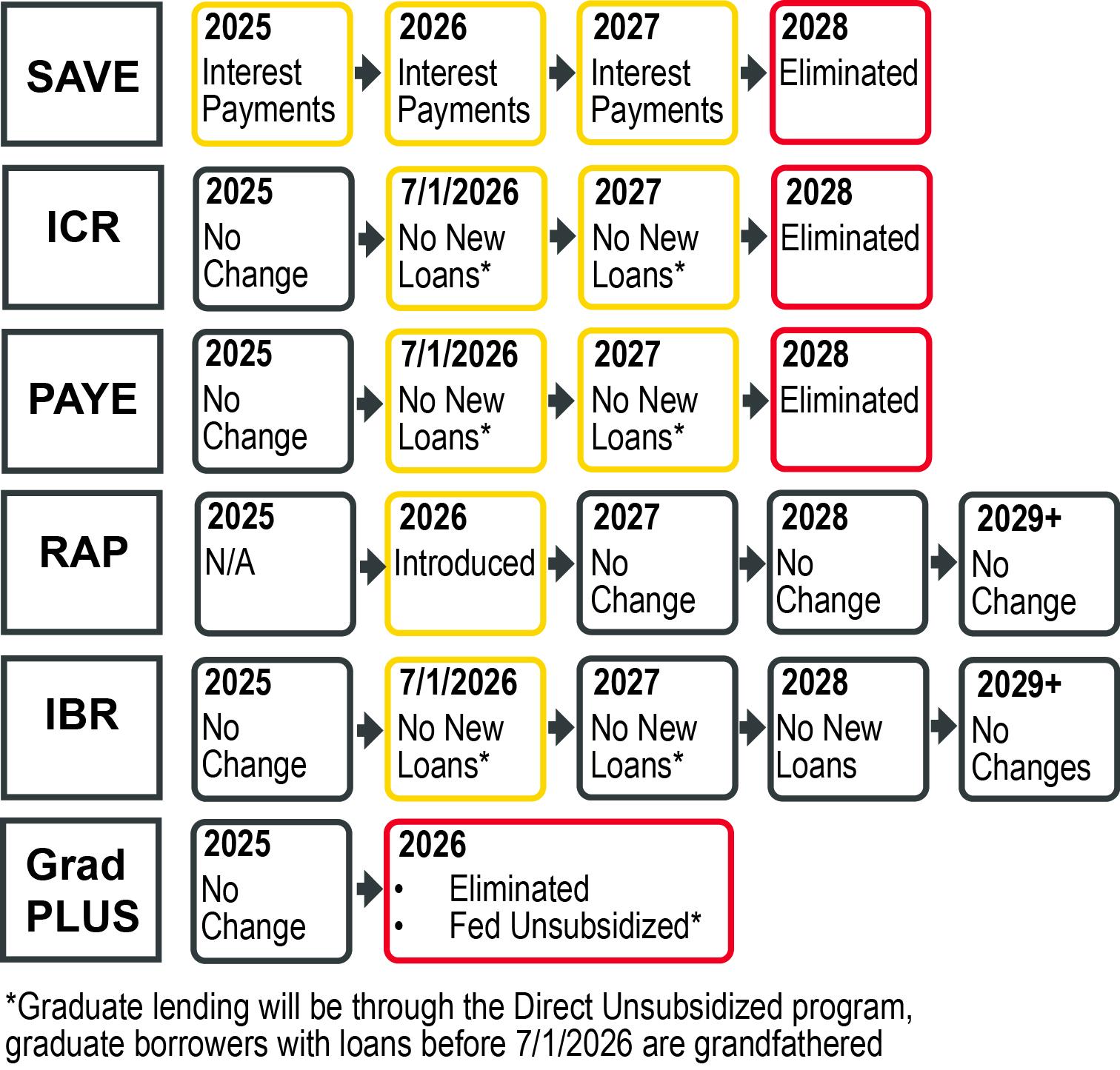

There are currently four income-driven federal student loan repayment plans (IDRs), and three balance-driven repayment plans. The income-driven plans are Income Based Repayment (IBR); Pay as you Earn (PAYE); Income Contingent Repayment (ICR); and Saving on a Valuable Education (SAVE). These plans differ primarily by minimum payment, percentage of income used to calculate payments, and forgiveness terms. SAVE replaced the Revised Pay As You Earn (REPAYE) plan in 2023 but was deactivated due to a court injunction. See “SAVE Plan, Forbearance, and What to Do” below for more information.

The three balance driven plans prior to July 2026 are: the Standard Repayment Plan (120 fixed payments); the em>Extended Repayment Plan (fixed payments up to 25 years); and the Graduated Repayment Plan (low initial payments, increasing every two years).

New in 2026

The new legislation consolidates these seven plans into two options. Starting in July 2026, new borrowers and existing borrowers who receive new loans will have two repayment plan choices: a new IDR called the Repayment Assistance Plan (RAP), or the Standard Repayment Plan. More details on these two plans are discussed in the next sections.

Note: Existing borrowers who have loans in repayment prior to July 1, 2026, can remain in their current income-driven repayment plan. If they are currently on a different plan, they can consolidate existing loans into the IBR plan and remain on that plan until the loan is paid off or forgiven. Previously, IBR required proof of financial hardship to qualify, but that barrier has been removed. It’s a good idea to use the Loan Simulator at StudentAid.gov to compare your options. If you choose to change plans, apply early, and be mindful of possible processing delays.

Repayment Plan Details for NEW Loans Disbursed on or After July 1, 2026

For loans disbursed after this date, borrowers will be limited to one of two choices.

(1) Standard Repayment Plan.

The Standard Repayment Plan combines all previous versions of the Standard and Extended plans. Borrowers will have fixed payments over 10–25 years, depending on the loan balance:

- 10 years for loan balances less than $25,000

- 15 years for loan balances between $25,000– $49,999

- 20 years for loan balances between $50,000– $99,999

- 25 years for loan balances $100,000 or more

Borrowers can shorten the duration of their loan by making larger or extra payments.

(2) Repayment Assistance Plan (RAP).

RAP is a new IDR plan which is scheduled to launch by July 1, 2026. Payments are calculated using the borrower’s adjusted gross income (AGI), with payments ranging from 1% to 10% of AGI, depending on income amount, with a minimum monthly payment of $10.00. It offers loan forgiveness after 30 years of payments and includes a small subsidy to reduce interest for low-income borrowers. Any loan balance forgiven after 30 years is taxable to the borrower as income. RAP is Public Service Loan Forgiveness (PSLF)-eligible (see below).

Good to Know

Adjusted Gross Income (AGI) is your total gross income from all sources (like wages, interest, and business income) minus certain specific deductions, such as student loan interest, educator expenses, and contributions to some retirement accounts. It’s a key figure on your U.S. federal tax return that determines eligibility for many tax credits, deductions, and benefits.

Repayment Plans and Income- Driven Repayment Forgiveness

The SAVE, PAYE, and ICR repayment plans for existing loans will be eliminated by July 1, 2028. Borrowers still in those plans after July 1, 2026, will need to consolidate to the new RAP plan to remain on an income-driven repayment plan. Borrowers who move to RAP will continue progress toward loan forgiveness. They can also switch to the standard repayment plan, but because the loan payment is calculated based on full repayment, there is no built-in forgiveness benefit.

The Income-Based Repayment plan will remain available for loans disbursed before July 1, 2026. It offers forgiveness after 20 or 25 years, depending on when your loans were issued, and it counts toward PSLF. Additional PSLF details are in the “About Public Service Loan Forgiveness” section below.

Graduate Student Loans: New Borrowing Limits

Starting July 1, 2026, all new federal lending for advanced degrees (graduate and professional school) will be from Direct Unsubsidized Loans. Most graduate students will be limited to borrowing up to $20,500 per year. An exception will be for specifically designated professional and licensure programs, which will have an annual limit of $50,000. The Graduate PLUS loan program will be eliminated for new borrowers after June 30, 2026.

Existing graduate or professional students who borrowed federal loans for their current program prior to July 1, 2026, remain eligible for Graduate PLUS Loans under a grandfathering provision, allowing them to continue borrowing at current rules to complete their program.

Good to Know

Graduate PLUS loans allowed students to borrow up to the full cost of attendance (minus other aid) and have no other specified dollar limit.

This typically applies for up to three additional academic years after July 1, 2026 (through roughly June 30, 2029), or until the end of their current enrolled program (whichever comes first), as long as they stay continuously enrolled in the same degree/ credential program without switching or starting a new one.

Good to Know

Specifically designated programs with an annual borrowing limit of $50,000 include:

- Medicine (M.D.)

- Osteopathic Medicine (D.O.)

- Dentistry (D.D.S. or D.M.D.)

- Law (J.D. or L.L.B.)

- Pharmacy (Pharm.D.)

- Veterinary Medicine (D.V.M.)

- Optometry (O.D.)

- Podiatry (D.P.M.)

- Chiropractic (D.C.)

- Clinical Psychology (Psy.D. or certain Ph.D. programs)

- Theology (M.Div. or similar)

- Similar licensure-based professional degrees. (undefined)

School Closures

If your school closes while you’re enrolled or shortly after you leave, you may qualify for loan forgiveness through the Closed School Discharge program. However, the rules have reverted to pre-2020 legislation. Automatic forgiveness is now paused, and borrowers must apply individually.

SAVE Plan, Forbearance, and What to Do

Starting in June 2024, many borrowers in the SAVE plan have been in administrative forbearance. During this time, no payments were required and no interest accrued. That changed on August 1, 2025, when interest obligations resumed. Principal payments are still not required, but borrowers can choose to make payments in two different ways. One is to make interest-only payments to keep loan balances from growing due to accumulated interest. The other choice is to make full payments (principal and interest) to pay down the loan balance. Any payments made should be directed to the loan servicer with instructions to apply them to interest or principal. However, these payments do not count toward Public Service Loan Forgiveness (PSLF) or Income-Driven Repayment (IDR) forgiveness during the forbearance period, unless retroactively applied via the PSLF Buyback option for qualifying borrowers.

About Public Service Loan Forgiveness

Public Service Loan Forgiveness (PSLF) is a federal program. Under PSLF, borrowers with Direct (Federal) Loans who make 120 qualifying monthly payments while working full-time for a qualifying public service employer, such as a government agency or 501(c)(3) nonprofit, can have their remaining loan balance forgiven.

In most instances, individuals in the SAVE or another IDR plan who are in forbearance are not earning time toward Public Service Loan Forgiveness or Income Driven Repayment forgiveness. To resume progress toward forgiveness, borrowers should consider switching to IBR, or RAP once it is available.

There is one main change coming to PSLF. Starting in 2026, any loan balance remaining and forgiven under PSLF will be taxed as income to the borrower. This brings PSLF terms in line with the other income-based loan forgiveness plans. There is also a proposal to exclude nonprofits whose operations violate federal law or engage in organizational discrimination from being considered as qualified PSLF employers. This proposal is still in negotiation at the time of this writing.

Parent Loans: Borrowing Limits and PSLF

Many changes are coming to Parent PLUS loans, but the loan program name will remain the same. First, there are new borrowing limits which will take effect on July 1, 2026. Parent PLUS loans will be capped at $20,000 per year and $65,000 total per student. Second, the repayment plan option for loans distributed after July 1, 2026, will be limited to the Standard Repayment Plan as outlined above.

Parent PLUS loans don’t qualify for PSLF on their own. Some parents with other student loans in addition to their PLUS loans could become eligible for PSLF. However, first the loans must be consolidated into a Direct Consolidation Loan. Once loans are consolidated, borrowers can enroll in IBR and start making qualifying payments toward PSLF. This option is only available until July 1, 2026, so it’s important to act well before that date to allow for processing time.

Action Steps - Summary

- If you’re affected by these changes, take action early. Use the Loan Simulator at StudentAid.gov to compare repayment plans.

- If you have Parent PLUS loans, consolidate them before July 1, 2026.

- If you’re in a plan that’s ending, switch to IBR before July 1, 2026, or RAP (when available in 2026) before July 1, 2028.

- If your school closes, submit your student loan discharge application as soon as possible.

- Each student borrower’s overall lifetime borrowing limit for federal student loans (excluding parent loans) will be $257,500. Plan accordingly.

- Private student loans have their own terms. The information in this document does not apply to private student loans, which often come with higher interest rates and fewer protections. It’s important to examine the terms carefully.

Timeline of Key Dates, Past and Future

August 9, 2024

Appeals court issues injunction blocking SAVE Plan components

July 4, 2025

One Big Beautiful Bill Act enacted, legislating student loan changes

August 1, 2025

Interest resumes for SAVE borrowers

July 1, 2026

RAP launches; new borrowing caps take effect

July 1, 2026

Deadline to consolidate Parent PLUS for IBR to qualify for PSLF

July 1, 2028

SAVE, PAYE, ICR end; IBR phased out

Graphic Timeline

DOROTHY NUCKOLS, MPH, AFC®

dnuckols@umd.edu

This publication, Federal Student Loan Reform 2025-2028: Your Guide to Repayment, Forgiveness, Borrowing Limits, and What You Need to Do (FS- 2025-0788), is a part of a collection produced by the University of Maryland Extension within the College of Agriculture and Natural Resources.

The information presented has met UME peer-review standards, including internal and external technical review. For help accessing this or any UME publication contact: itaccessibility@umd.edu

For more information on this and other topics, visit the University of Maryland Extension website at extension.umd.edu

University programs, activities, and facilities are available to all without regard to race, color, sex, gender identity or expression, sexual orientation, marital status, age, national origin, political affiliation, physical or mental disability, religion, protected veteran status, genetic information, personal appearance, or any other legally protected class.

When citing this publication, please use the suggested format:

Nuckols, D. (2026). Federal Student Loan Reform 2025-2028: Your Guide to Repayment, Forgiveness, Borrowing Limits, and What You Need to Do (FS-2025-0788). University of Maryland Extension. go.umd.edu/FS-2025-0788.